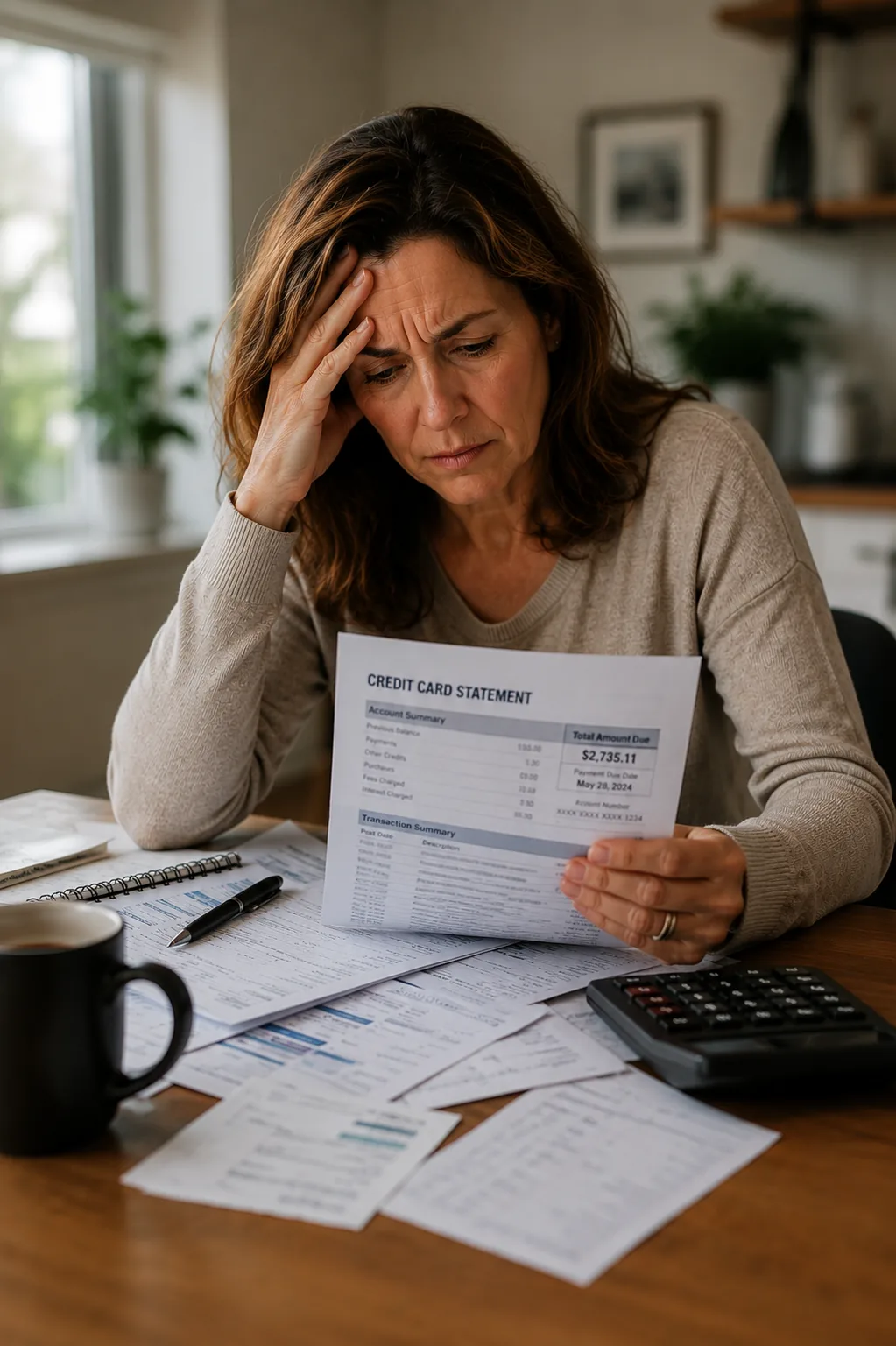

Debt isn’t the problem. The interest rate is.

If you’re carrying $40,000–$100,000+ in credit card debt, personal loans, or CRA arrears, you already know the math doesn’t work. At 21.99% interest, you’re barely treading water. A $60,000 balance costs over $1,100/month in minimum payments — and almost none of it goes toward the principal.

As a homeowner, you have an asset your bank won’t talk to you about. Your home equity unlocks rates as low as 6.99% — dramatically lower than any credit card or personal loan. The math changes completely.

Your home equity is working capital you’ve already built. Let’s put it to work for you — not against you.

Adjust the sliders below to estimate how much equity may be available to consolidate debt, access cash, or lower your monthly payments.

See how homeowners across Ontario, Alberta & Saskatchewan have used their home equity to eliminate debt, stop arrears, and lower their monthly payments.

$6,800

$71,900

$14,000

$92,700

$92,700

$102,500

$67,000

$29,000

$198,500

$198,500

$24,000

$28,000

$4,500

$56,500

$56,500

$64,000

$21,000

$217,000

$302,000

$302,000

$68,000

$19,000

$21,000

$108,000

$108,000

Certain details have been modified to protect client privacy while preserving the overall outcome.

Home equity consolidation works for virtually any type of consumer or unsecured debt. Here’s what homeowners most commonly consolidate through CreditReboot:

Home Equity Loan

Borrow a lump sum against the equity in your home. Ideal for debt consolidation, large expenses, or getting cash fast. Fixed rates from alternative lenders who focus on equity, not credit score.

HELOC with Bad Credit

A revolving line of credit secured by your home. Draw funds as you need them, pay interest only on what you use. Alternative lenders don’t follow traditional bank credit rules.

Second Mortgage

Borrow against your equity without touching your existing mortgage rate or terms. Fast approvals focused entirely on your equity position — not credit history.

Cash-Out Refinancing

Refinance your mortgage and pull out equity as cash — even with bad credit, a consumer proposal, or mortgage arrears. We find lenders who qualify you on property value, not your credit file.

Debt Consolidation

Roll high-interest credit cards, personal loans, and lines of credit into one low monthly payment secured by your home. Stop paying 19–29% interest and redirect that money toward rebuilding your financial foundation. Available even with damaged credit or past collections.

Alternative Mortgage

When the big banks turn you down, B lenders and private lenders offer real solutions based on your equity and property value — not a credit score. Private lenders move fast and approve based almost entirely on the equity in your home. CreditReboot works with both.

Both options can reduce what you pay monthly — but they work very differently and have very different long-term impacts on your finances.

Consumer Proposal

- Severe credit damage — stays on record 7 years

- Requires trustee involvement

- Process takes months

- Negotiate to pay less than you owe

- Option if no home equity available

Home Equity Consolidation

- No credit damage — actually helps rebuild credit

- Keep all your assets & property

- Approved and funded in days

- Pay off full balance at a lower rate

- Available even with bruised credit

“Parm was excellent — didn’t matter what our questions were, he always had time for us. Had a few tricky issues but everything was handled swiftly and professionally.”

“Parm was super knowledgeable and really helped us when we were in a pinch and needed a quick close. He made our stressful situation much more manageable. Would highly recommend!”

“I recently had the pleasure of working with Parm from CreditReboot, and I couldn’t be more satisfied with the experience. He worked tirelessly to find me a lender tailored to my needs.”

“Parm from CreditReboot is an absolute pleasure to work with. He specializes in home equity loans and second mortgages. Whenever I have a client who needs help, Parm is my first call.”

“No matter anyone’s predicament, especially in the current economic market, I highly recommend working with Parm and CreditReboot. They came through when no one else would.”

“CreditReboot, in particular Parm, is the most timely, honest, and professional broker I’ve ever had the pleasure of working with. I cannot recommend him highly enough.”

The Digital CreditReboot Process

No branch visits. No waiting in line. No unnecessary paperwork. Just a simple digital process.

-

1Pre-ApprovalFill this form, speak to the broker, get your quote.

-

2Application & ApprovalComplete the application, we shop the deal to 50+ lenders, choose your approval.

-

3FundingSign the broker documents, legal documents & get the funds!

9%

Related Reading: Second Mortgage Debt Consolidation in Calgary or Debt Consolidation Using Home Equity.

FAQ – Frequently Asked Questions about Debt Consolidation

Debt Consolidation by City

Each city page covers local home values, what consolidating actually costs there, and the questions we get asked most in that market.